What Are the Four Risk Management Strategies?

The four primary risk management strategies are risk avoidance, risk acceptance, risk reduction, and risk transfer. Together, these frameworks allow businesses to systematically manage, minimise, or bypass potential operational threats.

Risk is a part of life.

We cannot avoid it.

However, we can develop risk strategies to control and mitigate risk.

Key Takeaways: Risk Management Strategies

- The Four Pillars: Comprehensive risk management relies on four core approaches: Avoidance (eliminating the threat), Acceptance (retaining the risk), Reduction (limiting the impact), and Transfer (sharing the burden)

- Context Matters: There is no single best strategy. Bypassing a threat entirely (Avoidance) is ideal for high-impact dangers, while Acceptance is reserved for low-impact, inevitable operational costs

- Proactive vs. Reactive: Effective mitigation shifts an organisation from reacting to crises to actively lowering their probability and severity before they strike

- Cost-Benefit Balancing: Every strategy carries a trade-off. For instance, transferring risk via insurance protects capital but introduces ongoing premium expenses

What Are the Four Risk Management Strategies?

What Is Risk Avoidance by Elimination?

Risk avoidance is the deliberate operational decision to bypass a potential threat entirely by completely eliminating the activity, asset, or process that introduces the risk.

Prevention by elimination is the best way to mitigate risk. You are reducing the amount of risk you take. Risk avoidance is the decision to avoid accepting a risk that could harm a business or its assets. On the other hand, a risk management strategy is the method of controlling and mitigating the negative or positive consequences of potential risk events.

What Is Risk Acceptance?

Risk acceptance is a conscious management strategy where an organisation recognises a specific risk exists but chooses to take no protective action because the cost of mitigation outweighs the potential impact.

Assess, identify and accept risks. Risk assessment aims to determine the level of risk a business is willing to accept to achieve its objectives. Accepting risk is the decision to accept the potential consequences of a possible event.

All businesses use strategies for risk acceptance – governance, monitoring and reporting, crisis management, and insurance – to accept a specific risk.

Risk acceptance is a conscious decision to accept the consequences should a risk event occur.

Examples:

- Exchange rate: not taking out exchange forward cover is an example of risk acceptance. The impact will only be known when the order is placed

- Car insurance: You accept absolute risk by not having insurance on your car and not paying an insurance premium. You also accept the risk of funding a rental car and do not choose this option in exchange for a lower insurance premium. Alternatively, in exchange for a lower insurance premium, you accept some financial risk on the excess payment

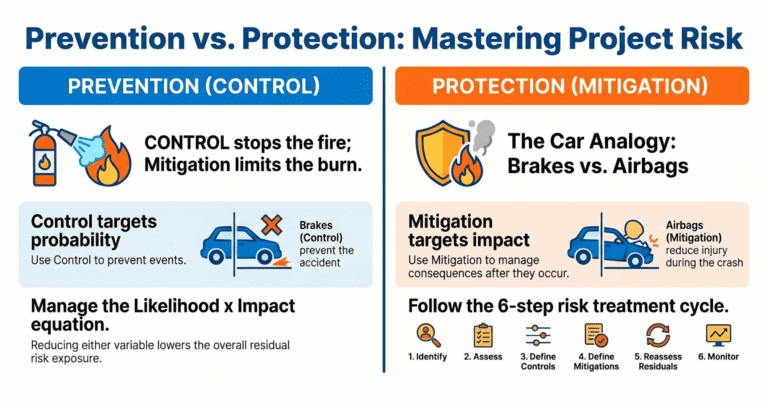

What Is Risk Reduction?

Risk reduction is the implementation of specific controls, protocols, or safety measures designed to lower the overall likelihood of a risk occurring or to minimise its severity if it does.

Risk management involves using information from risk assessments and other sources to make informed decisions about controlling and mitigating risks. Risk controls allow businesses to reduce or eliminate the chance that risks will cause harm.

Examples:

- Health and safety: workers must use Personal Protective Equipment (PPE) when in a particular area of a worksite

- Quality: a manufacturer reduces financial and schedule risk by the impact of rework by improving the quality assurance process

What Is Risk Transfer?

Risk transfer is a financial or contractual strategy where the burden of a potential risk is legally shifted from one organisation to a third party, typically via insurance policies or outsourcing agreements.

Transfer risk to other parties. Risk transfer is moving risk from one entity or organisation to another. It can reduce a particular business activity or protect other businesses from a risky decision.

Examples:

- Insurance: the insurance policy transfers risks such as flooding or fire to business premises

- Outsourcing: outsourcing a particular project or service and transferring the risk with the contract terms

What Is Contingency Planning?

What can you do when a risk becomes an issue? There are a few things that you can do to mitigate the risk of something going wrong.

Establish clear goals and objectives for the business, ensure all stakeholders are on the same page, and create a contingency plan that outlines what must be done to meet these objectives after a risk becomes an issue.

Additionally, the risk must be monitored throughout to identify any necessary changes or updates to the contingency plan.

Finally, communication protocols and procedures should be established if something goes wrong so everyone knows what to do and when.

Frequently Asked Questions

What are the four primary risk management strategies?

The four primary risk management strategies are risk avoidance, risk acceptance, risk reduction, and risk transfer. Together, these frameworks allow businesses to systematically manage, minimise, or bypass potential operational threats.

What is the difference between risk avoidance and risk reduction?

Risk avoidance completely eliminates a threat by halting the activity that causes it, resulting in zero risk exposure. Risk reduction, by contrast, accepts that the activity will continue but implements safety controls to reduce the probability or severity of an adverse event.

Why is contingency planning important in risk management?

Contingency planning is crucial because it provides an immediate, actionable roadmap for when a risk cannot be avoided or mitigated. It ensures business continuity and minimises operational downtime during an active crisis.

Conclusion

Managing risk is essential for any business.

The four risk strategies listed above and developing contingency plans can reduce your risk profile and keep your business running smoothly.